Wealth Without Shelter

How neoliberal policy made homelessness routine in the age of billionaires.

This Essay is written from an Australian perspective, drawing on lived experience and policy shifts over time, with reference to the United States as the most developed expression of these trends. In the United States, tent encampments now occupy public land within walking distance of billion‑dollar financial districts. Los Angeles alone has seen homeless populations rise alongside record wealth creation. The American case is not an outlier; it is the logic of neoliberalism pushed to its sharpest edge.

Opening

“There is no greater misery than to have no home.”— Euripides (c. 480 – c. 406 BC), Greek Tragedian

“Wealth and displacement now occupy the same ground.”

Homelessness now exists at a scale that would have been unrecognisable in the decades following the Second World War. Across wealthy nations, tent encampments, overcrowded shelters, and families without secure housing have become visible features of cities that generate immense wealth. This is not confined to the margins of poorer economies; it sits at the centre of affluent societies.

That was not the social landscape I grew up in. Born in 1950, in a working‑class suburb of Auckland, NZ, I never saw a tent city. I never walked past someone sleeping in a shop doorway as part of my routine. Through the 1950s, 1960s and into the 1970s, governments treated housing as a core obligation. Public housing was built at scale. Rents were regulated. Social security systems were designed to prevent extreme deprivation. Homelessness existed, but it did not define the urban environment as it does today.

That absence was not accidental; it was the result of policy.

The break comes with the rise of neoliberalism. From the late 1970s onward, governments shifted away from direct provision and toward market delivery. Housing moved from a public responsibility to a private asset base. The state reduced its role as a builder and expanded its role as an investment facilitator. Access to shelter became increasingly dependent on participation in the market.

At the same time, wealth expanded dramatically. This shift openly celebrated accumulation as a virtue, captured by the era’s cultural embrace of excess. That reordering did not remain confined to financial markets. It reshaped housing. Homes became assets. Multiple ownership expanded. Tax policy encouraged it. Credit enabled it. Wealth flowed into property not to meet need, but to secure return.

The contrast is now unavoidable. Wealth has increased. Asset values have risen. Financial markets have expanded. At the same time, housing insecurity has grown to the point where families live without the most basic conditions of stability.

This is the most visible measure of what has been lost. Housing did not fail; it was repurposed. It now functions efficiently as an asset, and poorly as a shelter.

I. The Welfare State: When Housing Was a Public Obligation

“Housing once formed part of the social contract: built, regulated, and treated as essential infrastructure.”

In the decades following the Second World War, governments across the developed world operated within a framework that treated social stability as a primary responsibility. This was the welfare state in practice: not an abstract idea, but a set of policies that placed housing, healthcare and education within the scope of public obligation rather than market outcome.

Housing sat at the centre of that arrangement. Governments did not rely solely on private markets to deliver it. They built it. Public housing programs operated at scale, providing affordable, secure accommodation for working families, the elderly and those on lower incomes. This was not a marginal activity; it formed a visible and accepted part of the housing system. Rent controls and regulatory frameworks reinforced affordability, ensuring that access to shelter did not depend solely on purchasing power.

The principle was clear. Housing was treated as a public good rather than a financial instrument. It was understood as essential infrastructure, as necessary to a functioning society as roads, schools and hospitals. Security was designed into the system. People were not expected to navigate housing risk alone, and the consequences of economic hardship were moderated through direct provision.

The outcomes reflected those choices. Home ownership expanded, but it did so alongside a safety net that reduced the risk of exclusion. Single‑income households were more viable. The cost of housing, while not insignificant, did not dominate household budgets as it does today. Most importantly, homelessness, while it existed, did not present itself as a widespread or defining feature of urban life. It was not normalised and was not accepted as an unavoidable condition in wealthy societies.

I did not experience visible displacement as a child or a young adult. No tent encampments occupied public parks near my home. No families I knew lived in cars or temporary shelters. That absence was not the product of chance or cultural difference. It was the result of policy choices that prioritised stability and access.

This is not an argument that the welfare state was without limitation. Inequalities persisted. Access was not uniform across all groups. Economic pressures remained. But the system was organised around a different set of priorities. It sought to reduce risk exposure rather than amplify it. It treated shelter as a requirement of social order rather than an opportunity for accumulation.

What existed in this period was not accidental. It was constructed, maintained and funded through deliberate political choice. That is what gives the comparison its weight. The conditions that prevailed were the product of policy, and they can only be understood in relation to the policy decisions that replaced them.

II. The Rise of Neoliberalism: From Public Provision to Market Control

“The Champions of Neoliberalism”

From the late 1970s onward, the policy framework that had underpinned the welfare state was dismantled and restructured. This shift is best understood through the rise of neoliberalism: a model that redefined the role of government, the function of markets and the purpose of public policy.

Neoliberalism did not emerge by chance. Its intellectual foundations were developed over decades, most prominently through the Chicago School of Economics, associated with economists such as Milton Friedman. The argument was consistent: markets allocate resources more efficiently than governments, and economic growth is best achieved by reducing state intervention, deregulating industry, and prioritising private enterprise.

Neoliberalism did not begin by celebrating greed. It elevated self-interest as the primary engine of economic life. Once embedded in policy, through deregulation, privatisation, and the weakening of public constraints, that principle expanded beyond theory into practice. What appears as greed at the social level is not an aberration but a logical outcome: an economic order structured to reward accumulation while limiting restraint.

The famous “greed is good” line from Gordon Gekko, the corporate raider in Wall Street, did not invent the idea. It distilled a reality already taking shape, one in which the pursuit of private gain had moved from being constrained to being openly celebrated.

The state, within this framework, was not removed. It was repositioned. Its role shifted from direct provider to market enabler, from builder to regulator, from guarantor of outcomes to manager of conditions.

These ideas were implemented most rapidly where opposition could be contained. In Chile, following the 1973 coup, the Pinochet regime adopted neoliberal reforms at speed: state assets were privatised, unions were suppressed, and public spending was reduced. The results demonstrated both the model’s capacity to generate growth and its tendency to concentrate wealth and increase inequality. By the early 1980s, the same principles were embedded in Western democracies. Thatcher in Britain and Reagan in the United States pursued privatisation, financial deregulation and confrontation with organised labour.

This was not a withdrawal of government authority. It was a reorientation. Policy settings were redesigned to favour capital mobility, investment growth and asset expansion. The language of governance changed accordingly. Terms such as efficiency, competition, and return replaced obligation, provision, and security.

Housing was directly affected. Under the welfare state, governments built and maintained housing stock as part of their social responsibility. Under neoliberalism, housing was repositioned within the market. Supply was expected to come from private development. Access became tied to purchasing power or participation in rental markets shaped by investment incentives.

At the same time, financial systems expanded. Credit became more accessible. Capital could move more freely. These conditions supported the transformation of housing into an asset class. Property was no longer simply a place to live; it became a vehicle for wealth accumulation, leveraged through borrowing and supported by policy.

The effects did not appear immediately. They unfolded incrementally. Public housing declined as a proportion of the total stock. Private ownership, particularly multiple ownership, increased. Prices rose in response to demand driven not only by need, but by investment.

The consequences of neoliberalism are now visible across multiple domains, but housing provides one of the clearest examples. When provision is replaced by market allocation, access is determined by capacity to pay. When policy supports accumulation, those with capital expand their position; those without face increasing barriers.

This is the structural shift that connects the welfare state to the present condition. Neoliberalism did not remove the system that preceded it; it redirected the balance between security and accumulation.

III. Housing as an Asset: The Engine of Inequality

“Homes became positions, portfolios, instruments of return.”

Housing did not fail; it was repurposed. It now functions efficiently as an asset, and poorly as a shelter.

Under neoliberalism, this transformation was constructed through policy, finance and incentives. Tax systems play a central role. In Australia, negative gearing and capital gains tax concessions reduce the cost of holding investment properties and increase the return on sale. Losses can be offset against income, while gains are taxed at reduced rates. These settings do not simply accommodate investment; they encourage it. Public revenue is used to support private accumulation.

Credit amplifies the process. Financial deregulation expanded access to borrowing, allowing individuals to leverage existing assets to acquire additional ones. Rising property values increase equity, which can then be used as collateral to purchase further properties. The cycle reinforces itself. Those already inside the market expand their holdings; those outside face escalating barriers to entry.

Multiple home ownership, once limited, is now normalised. Properties are not held for use; they are held for return. They sit alongside shares and other financial assets within portfolios. The language reflects the shift. Homes become “investments,” “positions,” “opportunities.” The function of shelter recedes behind the logic of growth. In the US, nearly 15% of homes are owned by investors; in Australia, the figure is comparable. The logic is the same.

This is visible in behaviour. Investors accumulate properties over time. Established owners convert gains into further acquisitions. The system does not restrain this process; it facilitates it. The consequences are cumulative. As capital flows into housing as an asset, a component of a property portfolio, prices rise. As prices rise, access narrows. Rent follows value. The cost of entry increases not only for ownership but for secure tenancy. The gap between those who hold property and those who do not widens with each cycle.

This is the mechanism through which inequality is produced within the housing system. It does not rely on land scarcity or the absence of construction. It is driven by the redirection of housing into an investment vehicle supported by state policy.

Under neoliberalism, there is no defined upper limit to accumulation. Wealth expands as long as the system supports it. At the same time, there is no guaranteed lower boundary for access to housing. Security is conditional, dependent on income, credit and market conditions. The system does not correct this imbalance; it reinforces it. As asset values rise, the political and economic incentives align to protect those values. Measures that would significantly reduce prices or limit accumulation encounter resistance, not because they are unworkable, but because they would alter the distribution of wealth.

The result is a housing system that operates effectively for those who own, and increasingly restrictively for those who do not. Public policy now subsidises the accumulation of housing as wealth, while failing to guarantee housing as shelter. This is the engine of inequality within the system.

IV. The Political Class: Power, Property and Contradiction

“The Political Class, who write the rules that reward them.”

The concentration of housing as an asset is not confined to private investors. It extends into the political class itself. Those who design tax policy, regulate housing and determine the level of public provision operate within the same system that rewards property ownership and asset accumulation.

This is not an accusation of individual misconduct. It is a structural condition. Members of parliament, across both major parties in Australia, hold investment properties. They participate in a housing market shaped by the very policies they oversee. A substantial proportion of federal parliamentarians own at least one investment property: many own more than one. This reflects the incentives embedded in the system: stable returns, favourable tax treatment and long‑term capital growth. The political class does not stand apart from these incentives. It responds to them in the same way as any other participant with access to capital and credit.

This is where the contradiction becomes clear. Those who write the rules participate in the rewards. They shape tax settings that influence property investment, including concessions that reduce the cost of holding multiple homes and increase returns on sale. They determine the level of public housing provision. They oversee regulatory frameworks that affect supply, planning and tenancy conditions. At the same time, they benefit from rising asset values within that system.

This is not incidental; it is structural. A system shaped by those who benefit from asset growth will tend to protect that growth. Measures that would materially reduce housing prices, expand public housing at scale or limit speculative accumulation carry political and economic costs. Those costs affect asset values, equity positions, and investment returns for those within the decision-making framework. The result is policy inertia. Reform is discussed, adjusted at the margins, or deferred. The underlying structure remains intact.

This alignment of interest does not require coordination or intent. It operates through shared incentives. When asset values rise, those holding assets benefit. When policy is considered, its impact on those values becomes a factor; the boundaries between public responsibility and private interest become blurred, not through corruption, but through participation.

The outcomes are visible. Those with the greatest access to capital and policy influence are positioned to acquire additional properties. Those without those advantages face rising barriers. Entry into the market becomes more difficult. Secure tenancy becomes less certain. At one end of the system, multiple homes are part of investment portfolios that generate returns. At the other end, individuals and families struggle to secure a single, stable place to live. Those who least need additional housing are those most able to acquire it.

This is not a failure of oversight. It reflects how the system is structured and who it serves. Those who write the rules participate in the rewards. That is not incidental; it is a structural contradiction.

V. The Lived Reality: The Losers in the System

“The lived reality: instability where stability once existed.”

The structure of the system is visible most clearly in its outcomes. It appears not in policy language or financial data, but in the lived conditions of those who exist at its margins.

I have seen this change across my lifetime. In the 1970s, when I was a young worker, a full‑time minimum-wage job could rent a modest flat in most Australian cities. Today, that same job will not cover the median rent in any capital city. People I grew up with were factory workers, clerks, and truck drivers who retired in the 2000s, having owned their homes. People I meet now in their thirties and forties, working two jobs, tell me they cannot see a path to secure housing, let alone ownership.

A recent report by ABC News Australia documented a family of thirteen living in makeshift tents, without sewerage, electricity, or stable shelter. Situations of this kind should not exist within a wealthy society. These are not conditions associated with resource scarcity. They emerge when access to resources is determined by position within the system rather than by need.

This is not an isolated case. It reflects a broader pattern. Individuals and families unable to secure housing move through temporary arrangements, overcrowded dwellings, short-term accommodation, and, increasingly, into visible homelessness. Stability is replaced by uncertainty. The capacity to plan, work, and maintain health is undermined by the absence of a secure base.

For those still within the system, pressure takes a different form. Workers take on multiple jobs to meet rising costs. Full‑time employment no longer guarantees stability. Income is absorbed by housing, leaving limited capacity for savings or resilience. Participation continues, but security weakens.

At the same time, another layer of the system operates through long‑term accumulation. Workers contribute over decades to superannuation funds, deferring income to secure retirement. These contributions form large pools of capital, managed and invested across global markets. The significance of these funds lies not only in what they provide to retirees, but in what they fund. Superannuation capital is integrated into the same financial system that shapes housing markets. It seeks a return. Property, infrastructure and financial assets generate that return.

The same superannuation pools that help bid up housing prices are also directed toward fossil fuel extraction, arms manufacturing, and defence contracting. A worker saving for retirement may unknowingly finance the very industries that destabilise the climate, displace communities, and supply the weapons of war. This is not an accident of investment; it is the logic of return maximisation operating without ethical or democratic constraint. The system does not ask whether capital should be allocated to public housing, a new gas field, or a weapons system. It asks only whether the return is sufficient.

The same capital, flowing through investment managers, simultaneously reinforces the asset logic that locks younger generations out of housing, funds the extraction that destroys the natural world, and equips the machinery of armed conflict. Workers are not hypocrites for participating; they have no realistic alternative. They are operating within a system they did not design. That structure ensures that the system reproduces itself. Capital grows, is reinvested, and contributes to rising insecurity, environmental breakdown, and militarisation, all from the same pool of deferred wages.

Governments retain the capacity to redirect this capital. They regulate superannuation systems and can prioritise sectors aligned with social outcomes – including social and affordable housing, renewable energy, and peaceful infrastructure. That capacity is not exercised at the scale required to alter the underlying structure. The system reproduces itself. Workers contribute. Capital accumulates. Investment flows toward return. Inequality, displacement, and destruction persist.

At one end, large pools of wealth sit within financial systems, expanding through investment. At the other end, individuals and families remain without secure shelter, while the same source funds the warming of the planet and world conflicts. This is not a failure of participation. It is the outcome of a system in which participation does not guarantee security, and in which the pursuit of return routinely overrides the most basic obligations to community and stability.

VI. Wealth Without Limit: The Question of Enough

“Nothing exceeds like excess.”

The system does not define an upper limit to accumulation. Wealth expands as long as the conditions that support it remain in place. There is no point at which additional ownership is considered sufficient, no threshold beyond which further acquisition is unnecessary. Capital grows, is reinvested, and grows again.

Not only housing, but the public services and rights essential to a functioning society are increasingly monetised. At the same time, there is no guaranteed lower boundary for access to essential needs. Housing is not secured as a baseline; it remains contingent on income, creditworthiness, and market conditions. What should function as a social guarantee is instead treated as a market outcome.

This creates a structural imbalance. Excess has no ceiling. Need has no floor. The issue is not that wealth exists. It is that its accumulation has no functional limit, while basic needs remain unsecured.

Under neoliberalism, accumulation is not restrained by necessity. It is enabled by policy. Tax systems, financial structures and investment frameworks are designed to support growth. Those with capital are positioned to expand it. Those without must enter the system under increasingly constrained conditions. This is not presented as an imbalance. It is presented as success. Wealth becomes a measure of achievement. Large holdings, multiple properties and significant financial portfolios are framed as indicators of individual success rather than as elements within a broader distribution.

This framing obscures the relationship between excess and exclusion. When capital is concentrated at one end of the system, access is restricted at the other. The issue is not simply that some have more. It is the structure that allows unlimited accumulation while failing to ensure minimum provision.

Inheritance does not resolve inequality; it extends it. The system moves in one direction. Wealth concentrates. Access narrows. The capacity to accumulate expands for some, while the capacity to secure basic stability shrinks for others. When excess operates without limit and need remains unmet, the balance between them is not neutral. It is structured.

This is the point at which the question of enough cannot be avoided, not as a moral abstraction, but as a practical consideration. If a system produces outcomes in which large concentrations of wealth coexist with visible deprivation, the issue is not the absence of resources. It is the absence of constraints on accumulation and the absence of a guarantee of provision. Under neoliberalism, both conditions are present.

Closing

The trajectory is clear. The welfare state established a framework in which housing, healthcare and education were treated as obligations of a functioning society. Neoliberalism restructured that framework. Provision gave way to market allocation. Security became conditional. Accumulation became central.

This is where the failure becomes visible. Walk along any city street, and the evidence is immediate: people sleeping in doorways, lives reduced to makeshift arrangements in the shadow of wealth.

The consequences are not abstract. Housing has been transformed into an asset class. Multiple ownership is encouraged and supported. Wealth concentrates through policy settings that favour investment and growth. At the same time, access to a single secure home has become increasingly uncertain for large sections of the population.

This is not a contradiction within the system. It is the outcome of it.

The political structure that oversees these conditions is not separate from them. Those who design and maintain the rules participate in the system they regulate. Policy reflects that alignment. Reform occurs at the margins, while the underlying framework remains intact. The same dynamic extends through the broader economy. Capital accumulates through financial systems, including the retirement savings of ordinary workers. That capital is directed toward sectors that generate return, reinforcing the structures that prioritise growth over provision.

What has emerged is not a lack of wealth, but a reordering of its purpose. Resources exist in abundance. Their distribution determines access. When allocation is driven primarily by return rather than need, outcomes follow.

Reversing this order does not require utopia. It requires three practical changes that are well within the capacity of a wealthy nation. First, phase out tax concessions for investment housing, negative gearing and capital gains discounts and redirect that revenue into public and community housing construction. Second, legislate a binding target for social housing as a proportion of total stock, returning to the post‑war commitment to direct provision. Third, require superannuation funds to allocate a mandated portion of their portfolios to affordable and social housing, turning workers’ capital toward their own security.

None of these measures is radical. Each has been implemented in other developed economies. Together, they would begin to shift the balance from housing as an asset back toward housing as shelter.

Until that order is reversed, the outcome will remain unchanged: multiple homes held as assets on one side, and families without one secure home on the other. Under these conditions, tent cities will grow, and more families will live in insecurity, fracturing the social contract that underpins a stable community. The wealth exists. The question is whether it will continue to serve accumulation or be redirected toward provision.

Don’t stay silent.

If this analysis matters, share it. If independent work matters, support it.

Silence is how unaccountable power becomes normal.

Refuse the comfort of indifference.

Subscribe for unfiltered analysis. Restack and share to widen its reach.

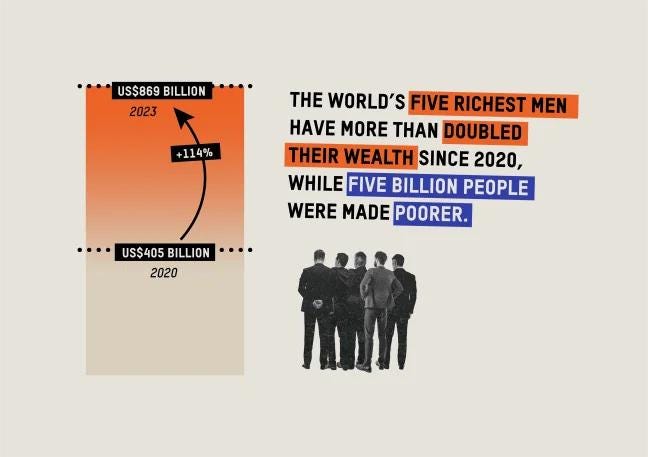

Draw Note:

Housing has become an asset class, evident on city streets where people sleep in doorways and makeshift setups shadow wealth. These conditions result from decades of policy choices, not chance. Housing was restructured and prioritized for profit over access, with clear evidence visible in everyday scenes.

Very interesting.